Georgia, Inland Waterways, National Category

Startup Uses Drone for Cleaning Water, Collecting Data

The nation’s sewers are estimated to be worth over $1 trillion and include nearly 17,500 wastewater treatment plants that operate to protect public health and ensure the well- being of communities. As the ability to detect and address emerging contaminants has improved, environmental regulations have tightened, and public opinion on pollution has changed, the wastewater sector is increasingly expected to produce advanced treatment outcomes, even as systems age. However, over the last decade, the sector’s renewal and replacement rate for large capital projects decreased from 3% to 2% while the average number of collection system failures for combined water utilities increased from 2 to 3.3 per 100 miles of pipe, indicating the impacts of aging infrastructure. The number of combined sewer systems has modestly decreased from 746 to 738 (2004 to 2023), and occurrences of sanitary sewer overflows have also decreased from 0.7 to 0.16 overflows per 100 miles of utility pipe (2015 to 2021). To fund these needs, the average bill for residential wastewater customers is increasing from $35 to nearly $65 per month from 2010 to 2020, but locally generated funds still fall short. In 2024, the wastewater and stormwater annual capital needs were $99 billion, whereas the funding gap was $69 billion, meaning only about 30% of the sectors’ infrastructure capital needs are being met. Assuming the combined wastewater and stormwater sector continues along the same path, the gap will grow to more than $690 billion by 2044.

rely on on-site wastewater systems

like septic systems

face new costs as they address

emerging contaminants

are designed with an average lifespan

of 40 to 50 years.

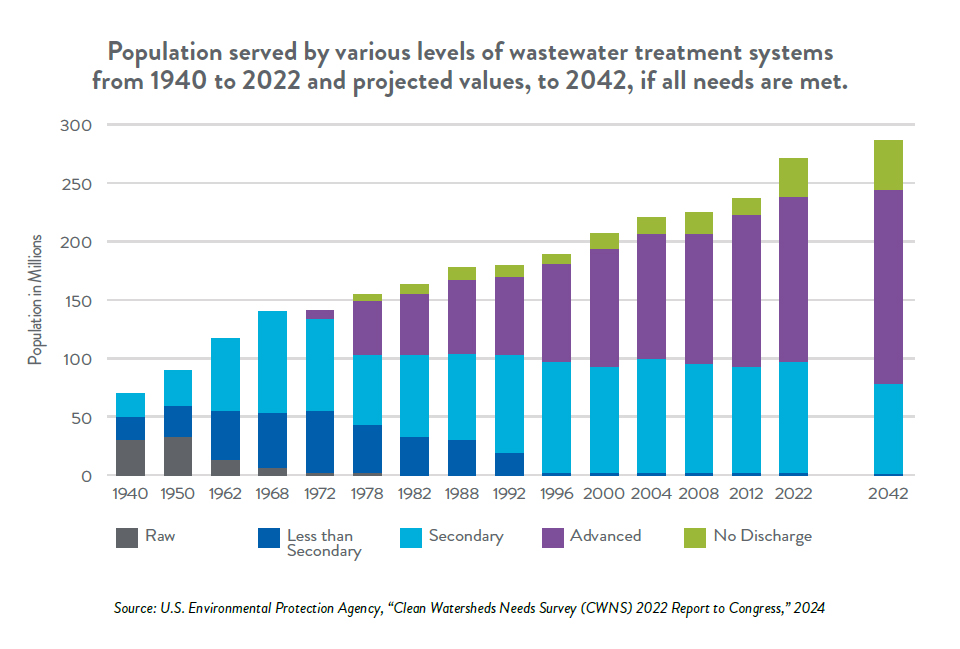

From 2012 to 2022, the number of publicly owned treatment works (POTW), or centralized wastewater treatment systems, increased from more than 16,000 to upward of 17,500 facilities of various sizes. According to the U.S. EPA’s 2022 Clean Watershed Needs Survey (CWNS), approximately 200 additional POTWs will come online by 2042. Of the existing centralized treatment plants, 38% currently provide advanced treatment, a number that is likely to increase to 42% over the next 20 years.

From 2012 to 2022, the number of publicly owned treatment works (POTW), or centralized wastewater treatment systems, increased from more than 16,000 to upward of 17,500 facilities of various sizes. According to the U.S. EPA’s 2022 Clean Watershed Needs Survey (CWNS), approximately 200 additional POTWs will come online by 2042. Of the existing centralized treatment plants, 38% currently provide advanced treatment, a number that is likely to increase to 42% over the next 20 years.

Over time, wastewater treatment systems are increasingly expected to produce advanced treatment capabilities owing to tightening environmental regulations, improved ability to detect and address emerging contaminants, and changing public opinion about pollutants, among other reasons. Over the next 20 years, these needs will be met by upgrading the level of treatment for some systems, and the rest of the needs will be met by constructing new treatment facilities. Some of these new or upgraded facilities are expected to be non-discharging, meaning the effluent is not released to surface waters but evaporated or beneficially reused (e.g., spray irrigation, groundwater recharge, or other purposes). By 2042, the EPA’s 2022 CWNS expects the population served by non-discharging facilities to grow by 21% or 8.8 million people.

Of the existing non-discharging facilities, 1% currently provide less-than-secondary treatment, 78% provide secondary treatment, and 21% provide advanced treatment.

However, not all communities depend on centralized wastewater treatment facilities. For some small communities and rural areas, on-site systems such as septic tanks or small, community systems are used to manage and treat wastewater needs. Since 2017, the portion of U.S. households using on-site systems has remained steady at nearly 1 in 5 or more than 66 million households.

Whether meeting the needs of urban or rural areas, wastewater conveyance systems provide critical service connections to homes, businesses, and communities. From 2019 to 2024, the combined length of urban and rural conveyance pipes has increased from 1.3 million miles to upward 1.87 million miles. Furthermore, since 2017, the measure of collection systems’ integrity (number of failures per 100 miles of pipe) for combined water utilities has been steadily hovering around two failures per 100 miles of pipe. However, in 2021, the value modestly increased to 3.3 failures per 100 miles of pipe, likely indicating the impact of the aging infrastructure.

The wastewater sector combines various forms of funding and financing to provide infrastructure systems and services that protect public health and the environment.

The wastewater sector combines various forms of funding and financing to provide infrastructure systems and services that protect public health and the environment.

Among these financial mechanisms, wastewater rates are critical for funding utilities. Although the average bill for residential wastewater customers is increasing from upward of $35 per month in 2010 to nearly $65 per month in 2020, it is not keeping pace with the growing costs for utilities to provide routine operation and maintenance (O&M) and preventative maintenance. At the same time, the average wastewater bill varies significantly across the country, and according to EPA’s affordability guidelines, which recommend spending around 2% of a household’s median income on sewer rates, more than 15% of the 50 largest cities (8 of 50) have rates that pose challenges for those who are economically disadvantaged.

Federal grants and additional financing options offer financial support for the wastewater industry. Since 2021, the federal government has taken significant strides to increase funding to the sector with the passage of the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA), wherein an additional

$46 billion over five years was provided to the water sector (drinking water, wastewater, and stormwater). In particular, the IIJA supported more than $11.7 billion in Clean Water State Revolving Funds (CWSRF), where 49% of funds were available for grants or principal forgiveness loans, 51% of funds were available for low- interest loans, and state matches were reduced from 20% to 10%. From Fiscal Year 2010–2021, annual appropriations averaged $1.6 billion annually for CWSRF. With IIJA funding, available funds will increase, from $1.9 billion in FY22, up to $2.6 billion by FY26.

Most IIJA funds to the wastewater sector were for loans and loan forgiveness, many of which emphasized support for disadvantaged communities. Therefore, IIJA did not provide significant additional resources to many utilities, particularly those in good financial standing, because when interest rates are favorable on the open market, it is easier to access bonds rather than take out a State Revolving Fund (SRF) loan.

Notably, IIJA is the first time Congress specifically directed funding ($1 billion over five years) to address emerging contaminants within the framework of eligible CWSRF activities. Over five years, the program received $100 million in the first year and $225 million each following fiscal year. Federal funding also increased to the Water Infrastructure Finance and Innovation Act (WIFIA) program, which provides credit assistance to particularly large, multisector infrastructure projects: starting at $69.5 million in FY22 and increasing to $72.3 million in FY24.

In 2024, ASCE’s Bridging the Gap economic study reported the water infrastructure (drinking water, wastewater, and stormwater) investment gap at $99 billion annually, up from the $81 billion estimated in ASCE’s 2021 “Failure to Act” report. Taking a closer look at only wastewater and stormwater values, the future needs become more apparent, and the gap is reported at $69 billion annually. This means about 30% of the nation’s total wastewater infrastructure capital needs are being met. Assuming the combined wastewater and stormwater sector continues along the same path, the gap will grow to more than $690 billion by 2044.

The value of wastewater and drinking water assets is nearly $1 trillion. Over the last decade, combined utilities’ renewal and replacement rates have hovered between 1.1%–2.0%. However, this is likely a significant underestimate when considering the projected costs for expanding asset management, extending the life of aging infrastructure, and addressing emerging contaminants such as per- and polyfluoroalkyl substances (PFAS). Current health advisories and uncertainty ahead regarding PFAS were the top concern among surveyed utility respondents of the American Waterworks Association’s 2023 “State of the Water Industry” report.

In general, assets are aging while the materials for upgrading or replacing components are becoming more expensive. Therefore, the wastewater sector has had to adapt by expanding its focus from capital investment programs to maximizing the abilities of existing systems to extend their performance. This requires a shrewd balance of higher operational costs while maintaining performance conditions, a challenge addressed through the efficient and effective use of data. In a 2023 survey, 65% of more than 450 surveyed utilities said they were using digital tools to meet their increasingly complex operation and maintenance needs. However, 54% of these utilities also noted that, though they are collecting data, it is not being effectively leveraged. In most cases, the commonplace digital tools being used to guide O&M efforts include geographic information systems (GIS), analysis of customer data and information, computerized maintenance management systems, and automated or advanced metering. However, other utilities are using more advanced approaches to operations and asset management through the adoption of digital innovations, including data science, artificial intelligence, digital twins, and various forms of scenario modeling.

In general, assets are aging while the materials for upgrading or replacing components are becoming more expensive. Therefore, the wastewater sector has had to adapt by expanding its focus from capital investment programs to maximizing the abilities of existing systems to extend their performance. This requires a shrewd balance of higher operational costs while maintaining performance conditions, a challenge addressed through the efficient and effective use of data. In a 2023 survey, 65% of more than 450 surveyed utilities said they were using digital tools to meet their increasingly complex operation and maintenance needs. However, 54% of these utilities also noted that, though they are collecting data, it is not being effectively leveraged. In most cases, the commonplace digital tools being used to guide O&M efforts include geographic information systems (GIS), analysis of customer data and information, computerized maintenance management systems, and automated or advanced metering. However, other utilities are using more advanced approaches to operations and asset management through the adoption of digital innovations, including data science, artificial intelligence, digital twins, and various forms of scenario modeling.

On the whole, widespread adoption of digital innovations is not yet prevalent in many utilities around the country because of constraints including resource limitations (48%), the use of legacy data and systems (45%), inadequate levels of funding (35%), and a lack of supportive leadership or guidance (35%). While digital O&M tools provide valuable data and process efficiency improvements, there are workforce impacts from streamlining these tools and implementing more automated treatment technologies. The U.S. Bureau of Labor and Statistics names automation as one of the causes of a 6% staffing decline in the industry by 2032, with other causes including routine job changes, retirements, and low recruitment. Overall, as digital approaches to asset management and monitoring as well as automated treatment technologies become more commonplace in the wastewater sector, it is important to build current and future workforce capacity along the way.

The total number of combined sewer systems (CSOs) has decreased slightly from 746 in 2004 to 738 municipalities across the country in 2024. Combined sewer systems collect rainwater runoff, domestic sewage, and industrial wastewater into one pipe and are vulnerable to overflowing in heavy rain events. Progress on uncoupling combined systems is slow, partly because many of these systems are in historic, densely populated areas, making the updates logistically complicated and expensive.

The total number of combined sewer systems (CSOs) has decreased slightly from 746 in 2004 to 738 municipalities across the country in 2024. Combined sewer systems collect rainwater runoff, domestic sewage, and industrial wastewater into one pipe and are vulnerable to overflowing in heavy rain events. Progress on uncoupling combined systems is slow, partly because many of these systems are in historic, densely populated areas, making the updates logistically complicated and expensive.

Starting in 2019, EPA’s enforcement efforts, which typically focused on roughly 200 of the largest CSOs, discontinued the requirement of annual reports on the status of addressing CSOs. Although municipalities are still required to collect water quality data related to their CSO discharges, the agency does not consistently collect, analyze, or publish data at a national level, which is necessary to evaluate the infrastructure’s impact on water quality.

Furthermore, as collection systems age and decline in condition, groundwater and stormwater enters the networks through cracks, joints, or illicit connections as inflow and infiltration. When wastewater collection systems are overtaxed, sanitary sewer overflows (SSOs) can occur. Occurrences of SSOs have decreased from 0.7 overflows per 100 miles of wastewater utility pipe in 2015 to 0.16 overflows in 2021.

Utility managers, wastewater treatment plant operators, engineers, and elected officials bring aspects of resilience into the foreground of the design, siting, and planning phases of their wastewater infrastructure. Because wastewater vulnerabilities vary by geographic location, type of treatment system, infrastructure age, and ownership status, there is no one-size-fits-all solution. For instance, some wastewater systems are in low- lying areas that are especially prone to the impacts of flooding, while others may be in drought-prone regions or areas with increasingly frequent wildfires. Rather than continuing to operate under a business-as-usual framework, some infrastructure decision-makers are shifting from solely focusing on short-term metrics like population growth, capacity demands, and affordability to incorporate long-term, resilience-related factors into planning such as sea level rise, frequency, intensity, and likelihood of natural disasters, cybersecurity threats, and post-interruption recovery time. To support this effort, in 2022, the Providing Research and Estimates of Changes in Precipitation (PRECIP) Act was signed and resources were provided to NOAA to update the probable maximum precipitation (PMP) estimates that have previously remained static over the past several decades. As new estimates are brought more in line with a changing climate, utilities will be better equipped to design the nation’s wastewater infrastructure for future conditions.

For more than a decade, the Institute for Sustainable Infrastructure has developed and improved upon a comprehensive sustainability framework and rating system for infrastructure projects. The goal of the assessment process is to help those working on implementing civil infrastruture projects (e.g., communities, municipal decision-makers, engineers) to do so holistically through the consdieration of sustainable, resilient, and equitable approaches. Currently in the U.S. there are nearly 30 projects that have been assessed with only three related to the wastewater sector. In an effort to better streamline sustainability-related innovations, organizations directly and tangentially supportive of the wastewater sector (e.g., the Water Environment Federation, American Public Works Association, the American Society of Civil Engineers, and the American Council of Engineering Companies) have crafted tools, fact sheets, and case studies to encourage the use of best practices and key features from the framework while the data-intensisve process continues to gain traction.

According to the Water Environment Federation, the Circular Water Economy “recycles and recovers resources within the water use and treatment cycle to maximize value for people, nature, and businesses.” This paradigm and practice exists through collaboration among public and private sectors to optimize and recover valuable resources from water and wastewater. Doing so enables these sectors to combat climate change and support economic development, among other outcomes. Circular water economy initiatives also keep products and materials in use, regenerates natural systems, and seeks to reduce waste and pollution.

Photo Attributions

Select your home state, and we'll let you know about upcoming legislation.

"*" indicates required fields

Back